Wealth And Economic News This Week (2-Minute Read)

-

-

Published Friday, August 10, 2018 at: 7:00 AM EDT

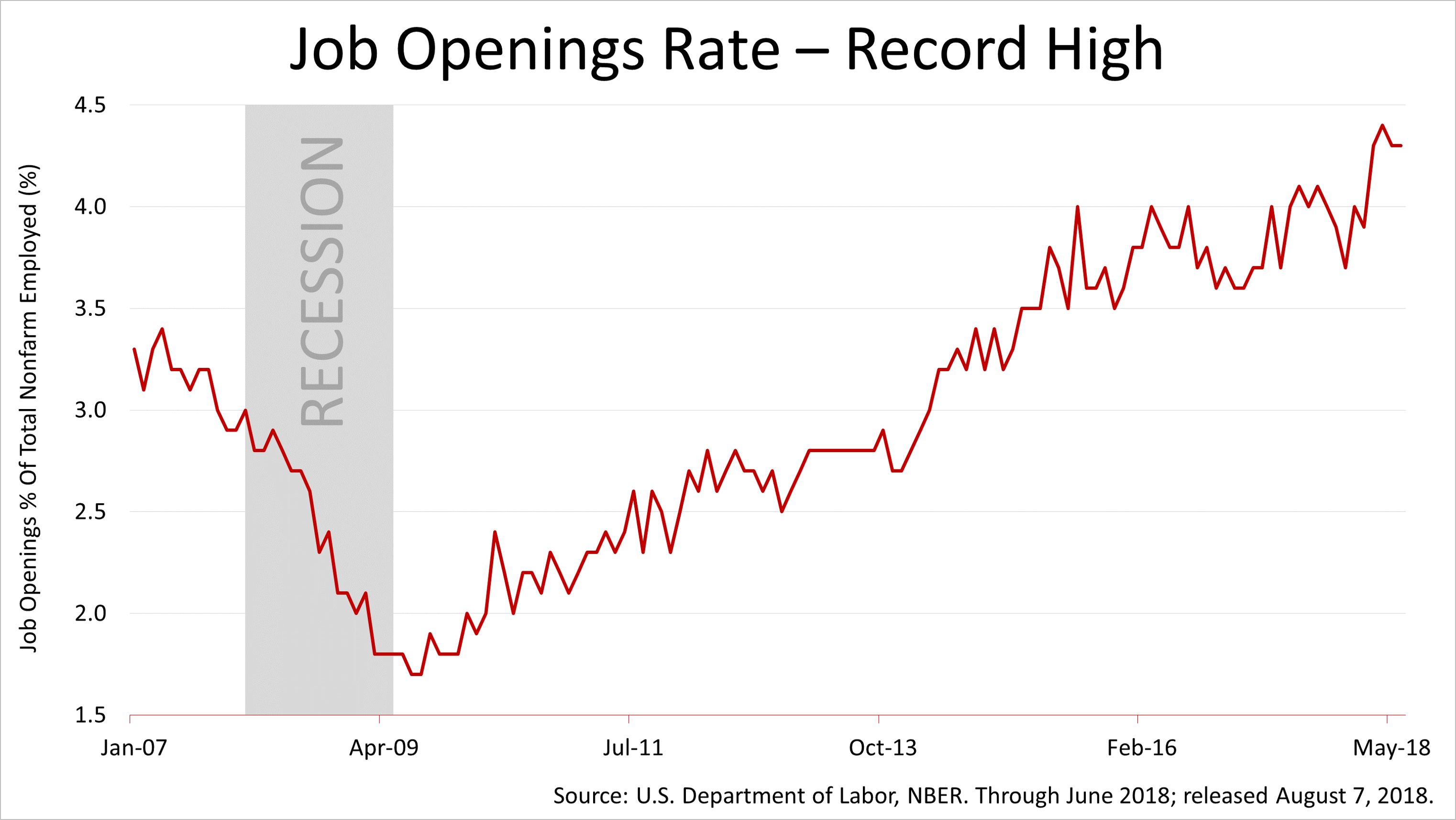

Job openings in June remained near a record high, and unemployment at a record low, while evidence of a tightening labor market grew.

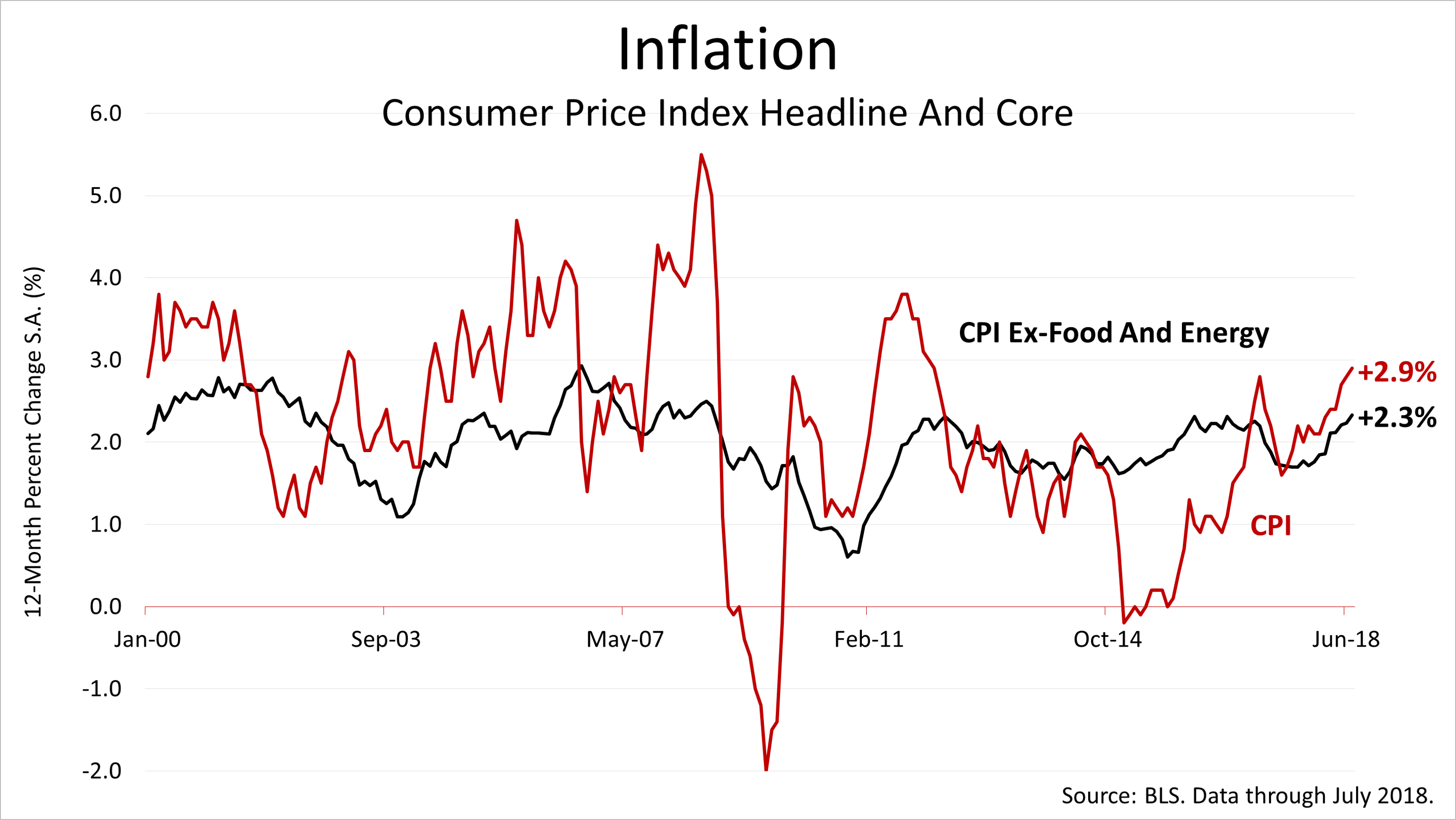

The core inflation rate, which excludes volatile food and energy prices, ticked higher in July, from 2.2% to 2.3%.

The steady rise in inflation in recent months has been expected by The Federal Reserve, and interest rate policy is expected to remain the same. The Fed has said it expects to raise rates once a quarter in 2018.

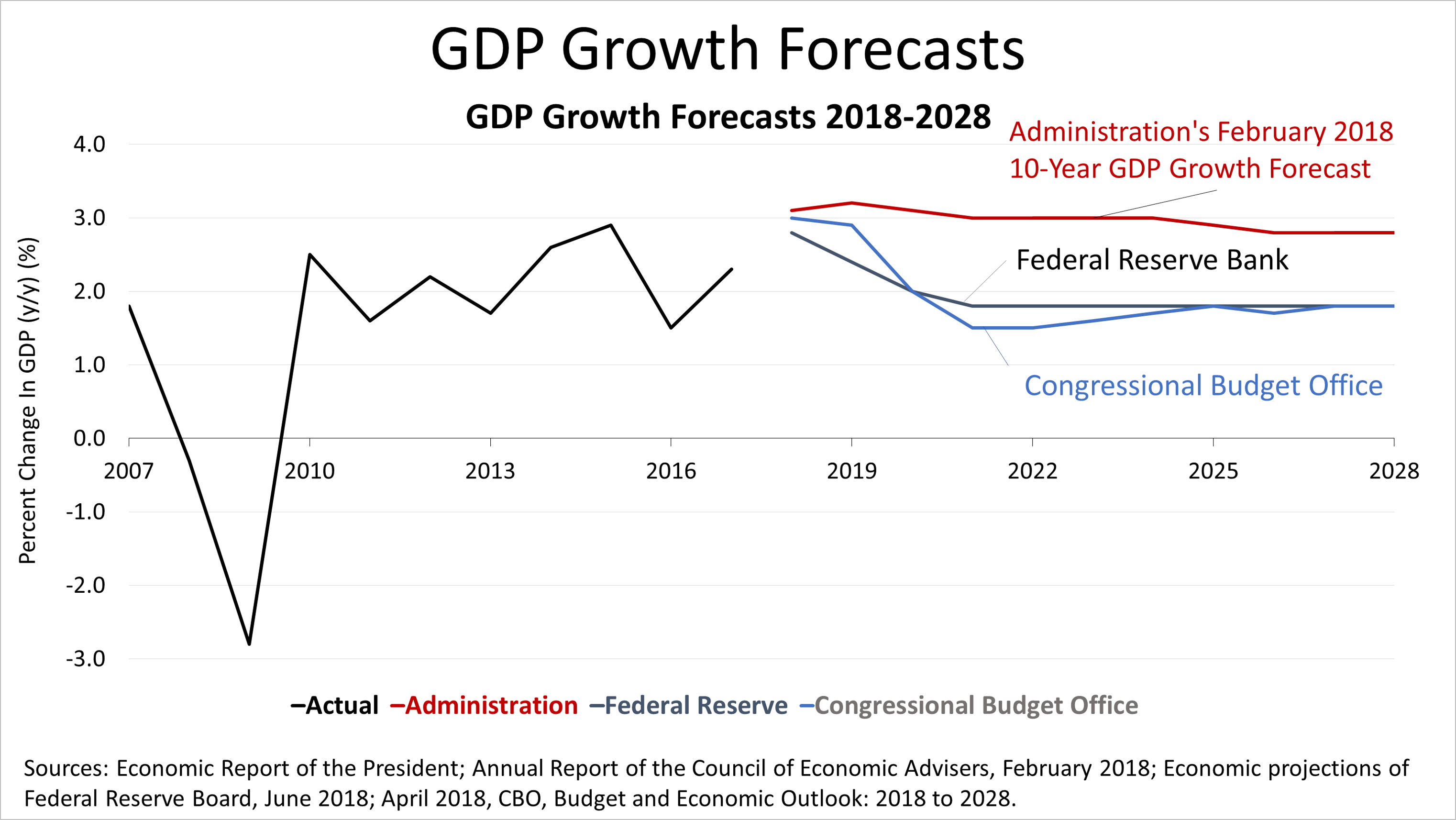

According to this month's survey of 57 economists conducted from August 3 to August 7 by The Wall Street Journal, the average growth rate estimated for 2018 increased to 3%. That was up from projections of 2.9% last month and 2.4% a year ago. The average growth rate for 2019 was 2.4%. By 2020, the average forecaster projects economic growth will slow to 1.8%, down from estimates earlier this year of 2%.

The Federal Reserve's economic forecast as well as the forecast from the non-partisan Congressional Budget Office and private economists surveyed monthly in The Wall Street Journal are all in agreement: the long-term rate of growth for GDP is about 2%.

However, the Trump administration's forecast for GDP growth in February, the most recent data available, is much more optimistic due to expectations about supply-side economics. Most economists remain skeptical about the boost in growth that will come from recent tax cuts. While the predominant view of economists is not as exciting, it is sustainable. The 110-month long expansion is, thus, poised to become the longest expansion in post-War history in July 2019.

This article was written by a veteran financial journalist based on data compiled and analyzed by independent economist, Fritz Meyer. While these are sources we believe to be reliable, the information is not intended to be used as financial advice without consulting a professional about your personal situation. Indices are unmanaged and not available for direct investment. Investments with higher return potential carry greater risk for loss. Past performance is not an indicator of your future results.

This article was written by a veteran financial journalist based on data compiled and analyzed by independent economist, Fritz Meyer. While these are sources we believe to be reliable, the information is not intended to be used as financial advice without consulting a professional about your personal situation. Indices are unmanaged and not available for direct investment. Investments with higher return potential carry greater risk for loss. Past performance is not an indicator of your future results.

2022

-

Despite Bad Economic News, Stocks Rose 4% In The Week Ended July 29, 2022

Despite Bad Economic News, Stocks Rose 4% In The Week Ended July 29, 2022

-

Amid Bad Data Releases, Leading Economists Predict No Recession

Amid Bad Data Releases, Leading Economists Predict No Recession

-

Good News: Real Retail Sales Dropped Fractionally In The Past Year

Good News: Real Retail Sales Dropped Fractionally In The Past Year

-

Financial Economic News Analysis

Financial Economic News Analysis

-

Odds Of A Soft Landing Shrunk After Friday's News

Odds Of A Soft Landing Shrunk After Friday's News

-

Bad Inflation Surprise Sends Stocks Down Sharply

Bad Inflation Surprise Sends Stocks Down Sharply

-

It Could Be A Long, Hot Summer For Investors

It Could Be A Long, Hot Summer For Investors

-

What A Difference A Week Makes

What A Difference A Week Makes

-

Amid Stock Market Turmoil, +2.3% Growth Projected In 2022

Amid Stock Market Turmoil, +2.3% Growth Projected In 2022

-

Staying On Track Amid The Ukraine And Inflation Crises

Staying On Track Amid The Ukraine And Inflation Crises

-

For Investors, 2022 Is Turning Into A Test

For Investors, 2022 Is Turning Into A Test

-

Is The Economy Brightening? Or Is The Federal Reserve Slamming The Door On Growth

Is The Economy Brightening? Or Is The Federal Reserve Slamming The Door On Growth

-

Perspective Amid A Moment Seeming Fraught With Investment Risk

Perspective Amid A Moment Seeming Fraught With Investment Risk

-

Two Years After The Pandemic Began

Two Years After The Pandemic Began

-

Turning The Page On A Dark Period In History

Turning The Page On A Dark Period In History

-

Russia-Ukraine War Erupted And Inflation Worsened But Outlook Drove Stocks Higher For The Week

Russia-Ukraine War Erupted And Inflation Worsened But Outlook Drove Stocks Higher For The Week

-

Investment Perspective Amid Risks Of Fed Tightening, Covid Variants, And European War

Investment Perspective Amid Risks Of Fed Tightening, Covid Variants, And European War

-

S&P 500 Lost -1.9% Friday; Latest U.S. Economic Data Are Strong

S&P 500 Lost -1.9% Friday; Latest U.S. Economic Data Are Strong

-

January Job Formation Figures Crushed Expectations, Amid A Shortage Of Workers

January Job Formation Figures Crushed Expectations, Amid A Shortage Of Workers

-

S&P 500 Closed Up 2.4% Friday After A -10% Correction

S&P 500 Closed Up 2.4% Friday After A -10% Correction

-

Stocks Declined Sharply, Even As Economists Expect 3% Growth In 2022

Stocks Declined Sharply, Even As Economists Expect 3% Growth In 2022

-

Should You Care About Wall Street Stock Market Predictions?

Should You Care About Wall Street Stock Market Predictions?

-

Weekly Economic Update For Investors

Weekly Economic Update For Investors

")