Featured News

Email This Article To A Friend

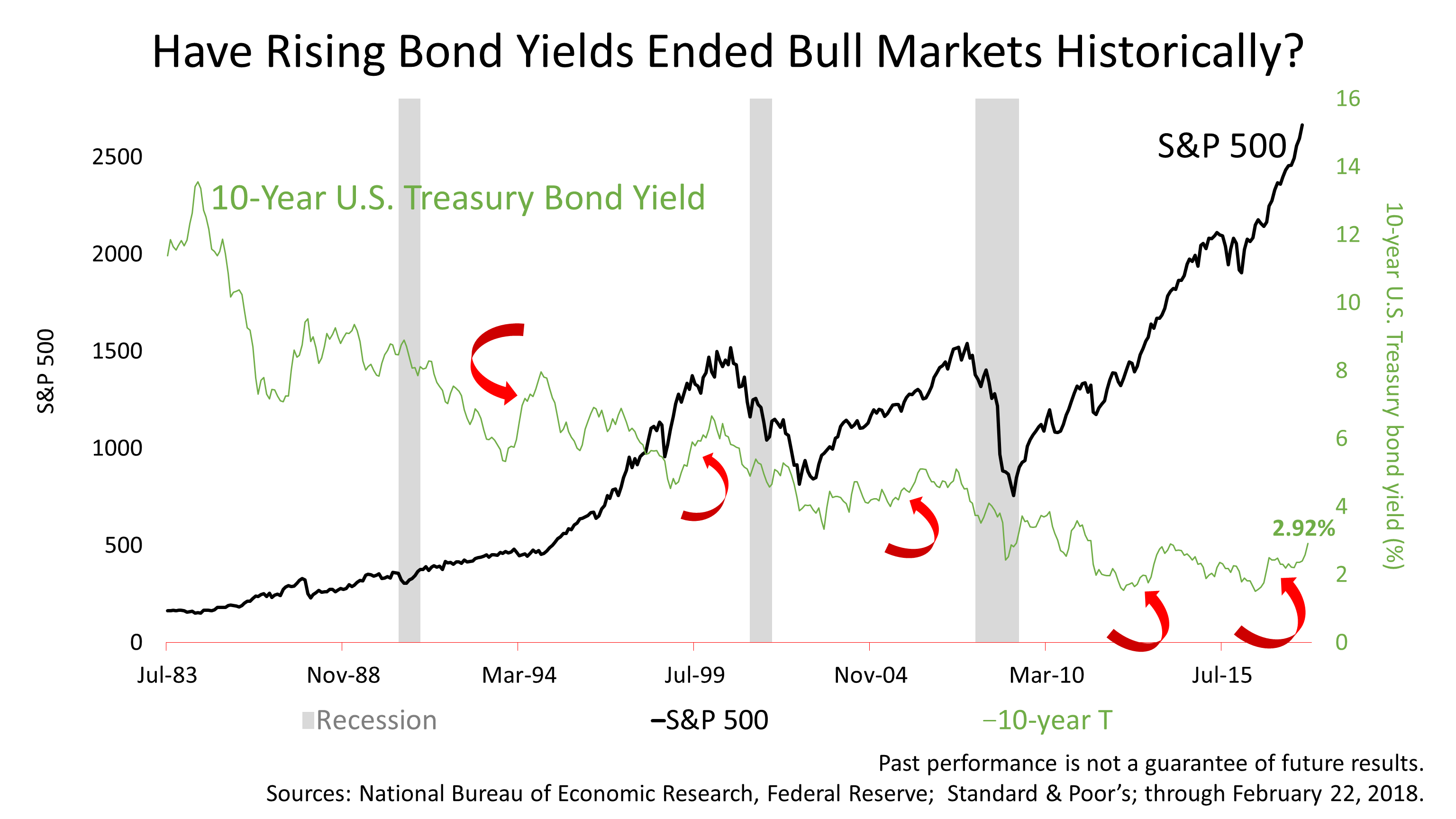

Will Rising Bond Yields Be Bad For Stocks?

Rising bond yields historically haven't been bad for stocks. While you may see stories in the financial press saying otherwise, the facts show that periods marked by rising bond yields have often coincided with bull markets in stocks.

The red arrows point to five periods since the 1990s when the yield on the 10-year U.S. Treasury bond rose sharply and stock prices also rose.

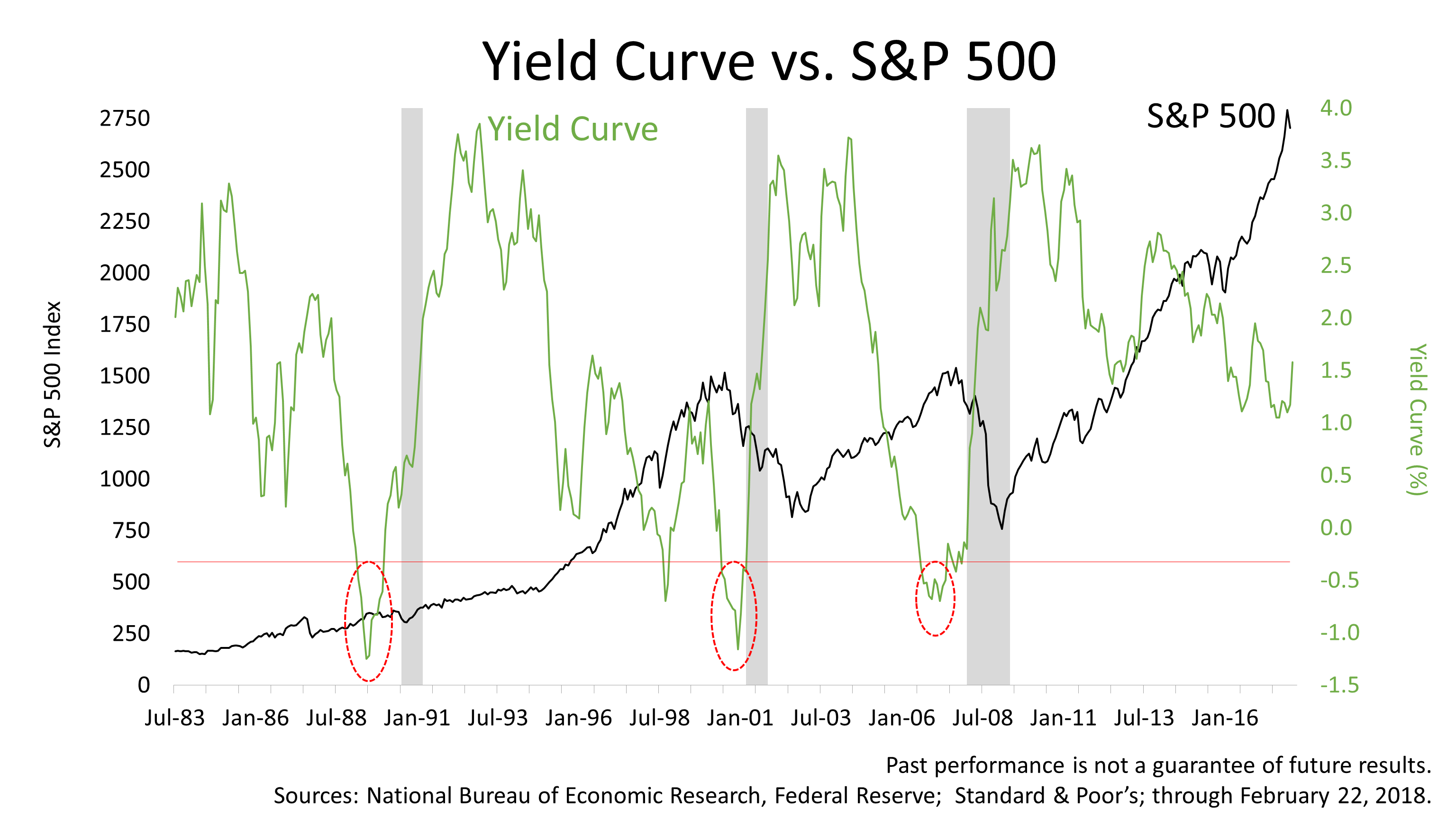

The key to stock prices and yields rising at the same time is the shape of the yield curve. That is the difference between long-term term bond yields and short-term interest rates. A negative yield curve is what has toppled stocks. When short term rates are higher than long-term yields, that is what hurts economic growth. The red circles show how the negative curve preceded the last three recessions. Currently, the yield curve is not near inversion, which is means the economic expansion eight-and-one-half year expansion could continue and the bull market in stocks could continue.

Economic growth is manifested in profits of publicly-held companies and largely determines how stocks are valued.

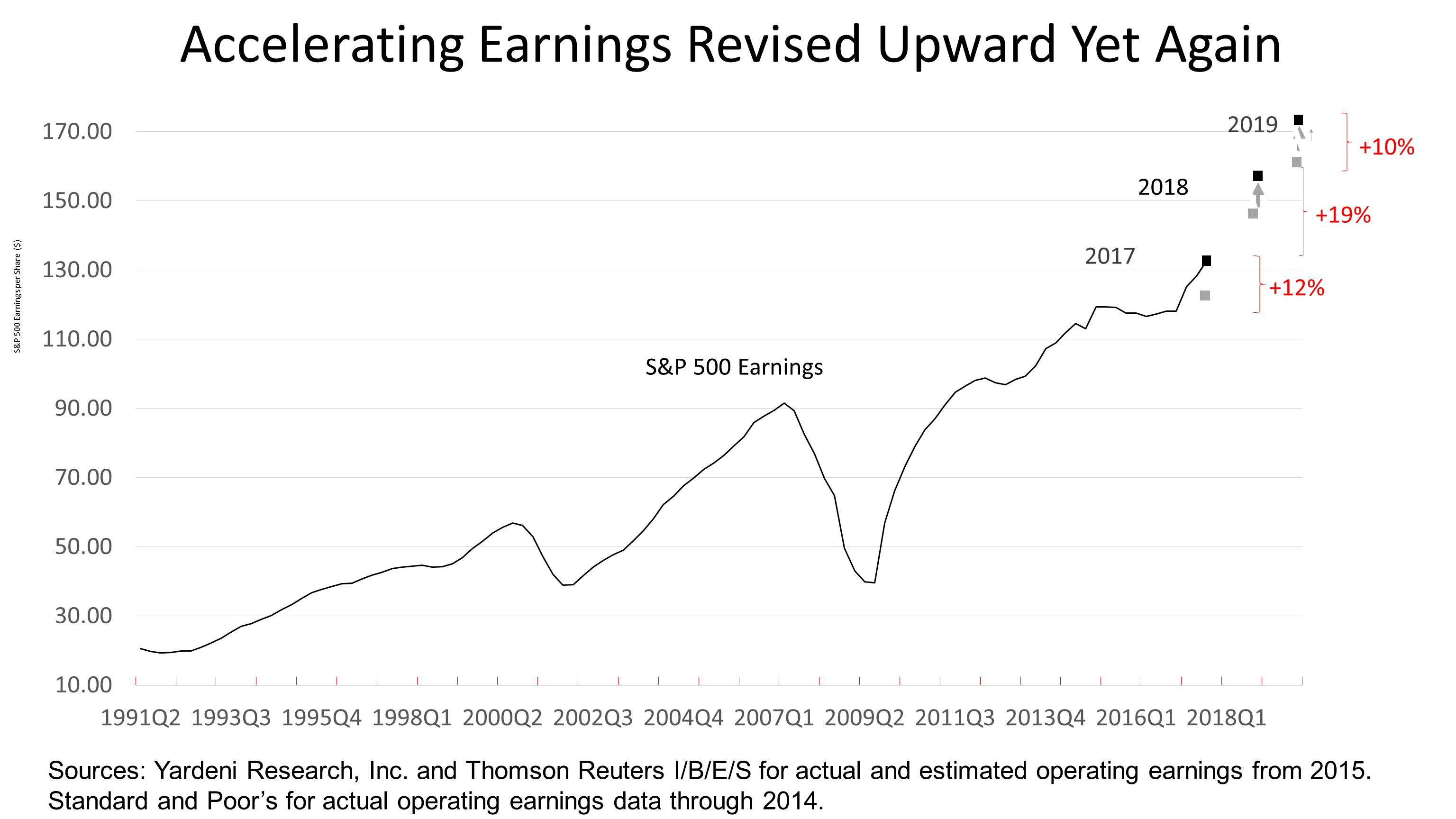

Profit expectations for the Standard & Poor's 500 companies, the largest U.S. public companies, grew sharply in just the past two weeks, continuing a pattern mentioned in weekly updates repeatedly over the last two months.

When the tax law was signed on December 22, 2017, the average company in the S&P 500 was expected to earn $131 a share in 2018 when the tax bill was signed on December 22, but that was revised to $157.47 and could be boosted again. S&P 500 operating earnings per share as of February 17, 2017 were $132.59 for 2017, $157.47 in 2018, and $173.93 in 2019, according to data from Yardeni Research, Inc. and Thomson Reuters I/B/E/S. Since the signing of the tax law according to independent economist Fritz Meyer, this chart shows the changing expectations for earnings.

Profits at S&P 500 companies historically have grown 7.4% annually over recent decades, and that has propelled stock prices to return an average annually of 7.4%. The expected growth in earnings of 12% when the final tally is done for 2017, is a lot higher than 7.4% -- as is the 19% growth rate in profits expected for 2018 and the 10% rate of growth projected profits for 2019, which is based on consensus earnings forecasts by Wall Street analysts.

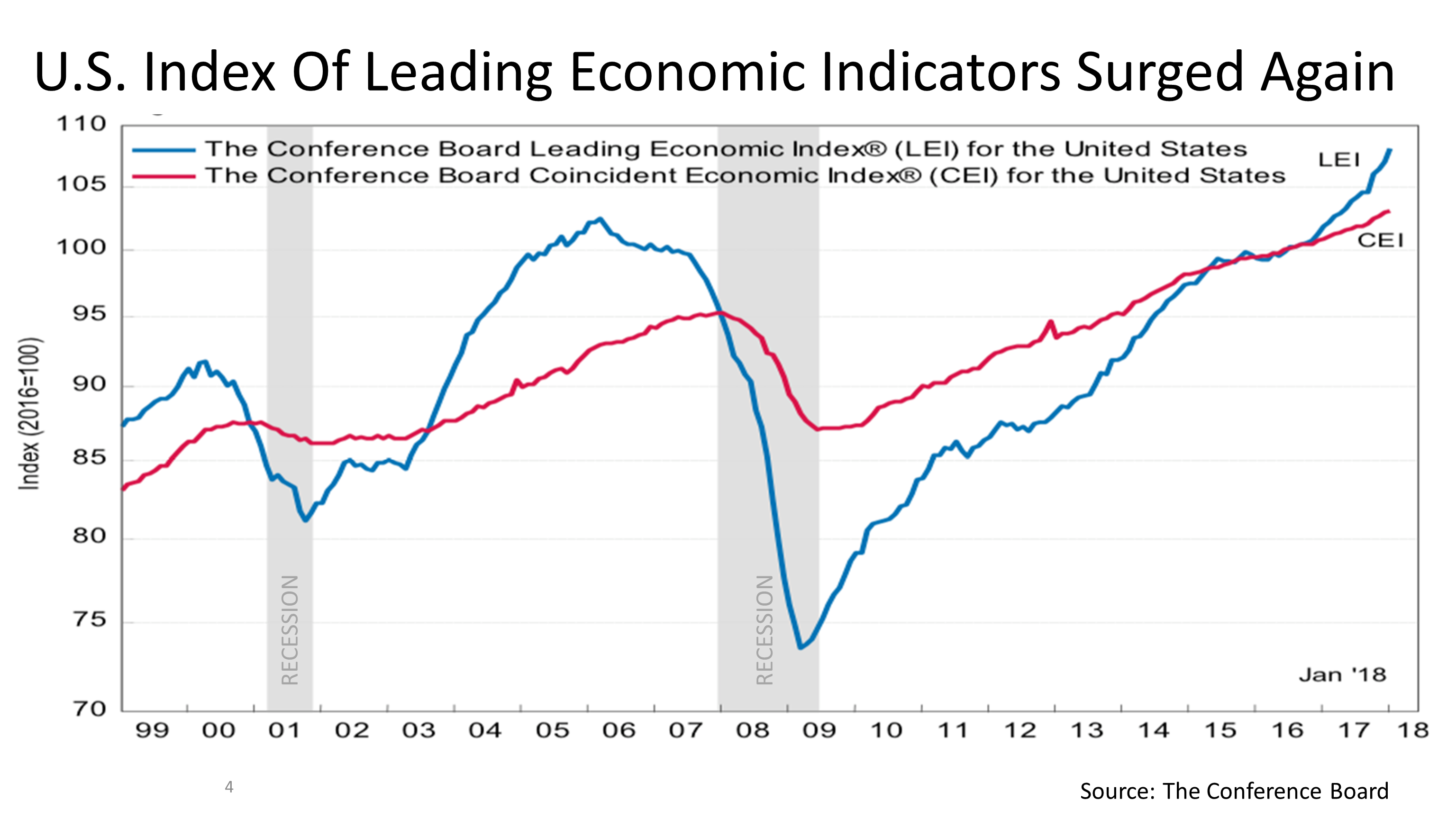

If all this good economic news was not enough, the leading indicators for the U.S., a forward looking composite of 10 economic indexes, were released on Thursday, and they strengthened by 1% in January to 108.1, following a 0.6% increase in December, and a 0.4% increase in November. The LEI is higher than it has been since 1999."The U.S. LEI accelerated further in January and continues to point to robust economic growth in the first half of 2018," according The Conference Board, an association for the nation's largest corporations not prone to hyperbole. "The leading indicators reflect an economy with widespread strengths coming from financial conditions, manufacturing, residential construction, and labor markets." This chart shows how the LEI has definitively rolled over well in advance of the last two recessions. Nothing like that is happening now. The Standard & Poor's 500 closed Friday at 2747.30, which was a 1.6% surge for the day and 0.6% higher than a week earlier.

This article was written by a veteran financial journalist based on data compiled and analyzed by independent economist, Fritz Meyer. While these are sources we believe to be reliable, the information is not intended to be used as financial advice without consulting a professional about your personal situation.

Indices are unmanaged and not available for direct investment. Investments with higher return potential carry greater risk for loss. Past performance is not an indicator of your future results.