Our team of advisors just spent several hours discussing IRMAA and honing strategies to deal with this pest.

No, I didn’t misspell it, and I’m not referring to Erma Bombeck or a great great aunt of mine. This is the Income Related Medicare Adjustment Amount. Simply put, the more income on your tax return in retirement, the more you will pay for your Medicare Part B and Part D prescription drug premiums.

It can ambush you in retirement. A large capital gain or IRA withdrawal could trigger the extra premium. A little planning may help avoid paying that extra premium. You can also appeal your situation if you have an unusual or non-recurring event.

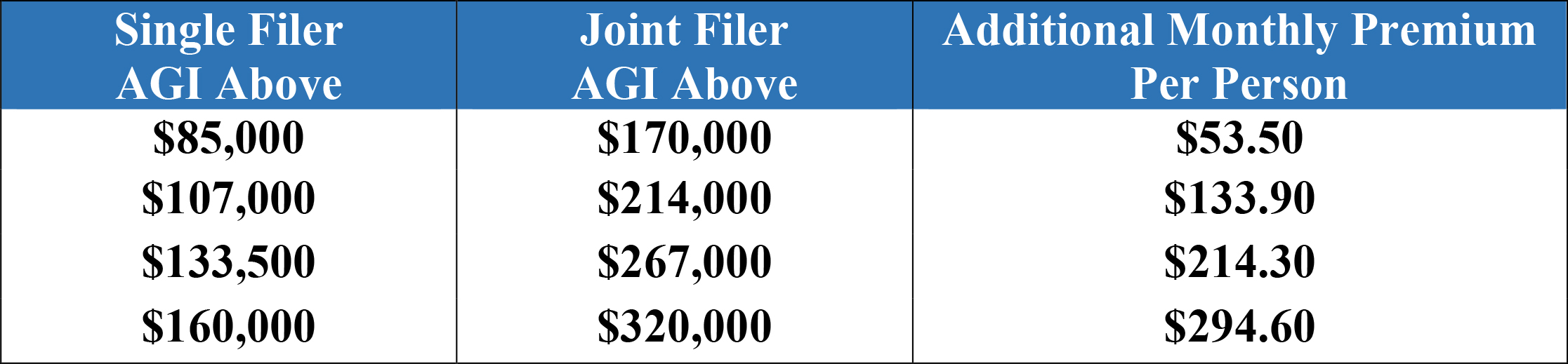

In 2018, you could pay as much as $294.60 in additional premiums if your income is too high. It’s a sliding scale that begins with single filer income above $85,000 or joint filer income above $170,000. If you use our Portfolio and Financial Planning Monitoring Service—we watch these levels for you and help you avoid paying more premiums than necessary—you usually don’t see this work, but it benefits you and your family. Our goal is to keep your income below the threshold each year.

Tax planning for retirees can often be more complicated than tax planning during the working years. We have to take into consideration:

- Required Minimum Distributions (RMDs) from your pre-tax accounts

- The sliding scale of taxability of Social Security benefits

- Limits for tax-free treatment of dividends and long-term capital gains

- Sale of a second home

- Plus much more

Many financial planners are not qualified to offer such tax planning advice. The Certified Financial Planning® Professionals of Phase 3 Advisory Services spend hours every year honing our skills in order to minimize your taxes throughout retirement.

It’s not as simple as trying to pay as little tax as possible today. It requires lifetime tax projections that include looking down the road for the “gotchas” of:

- Increasing Required Minimum Distributions (RMDs)

- Increased taxability of Social Security

- Additional premiums on Medicare

One useful tool we use is the QCD or Qualified Charitable Distribution. This IRS rule allows you to gift your Required Minimum Distribution directly to a charity and thereby avoid increasing your adjusted gross income. As a result, you also don’t claim the charitable contribution as a deduction on your itemized deductions. But by lowering your adjusted gross income on the front of the Form 1040, you increase the deductibility of your medical deductions and may avoid paying the additional Medicare premium under IRMAA rules.

Thresholds for 2018 are:

Be sure to let us know if you receive the notice from the Social Security Administration that you are subject to these higher premiums. NOTE: If your income triggers the IRMAA rules due to an unusual event (such as the sale of a second home), you may be able to appeal the higher premium.